CFO / Group Finance use case

Fraud Detection & Financial Controls Monitoring

Safeguard assets by automatically detecting anomalies in financial transactions and enforcing internal controls in real-time.

- Easy setup, no data storage required

- Free forever for core features

- Simple expansion with additional credits

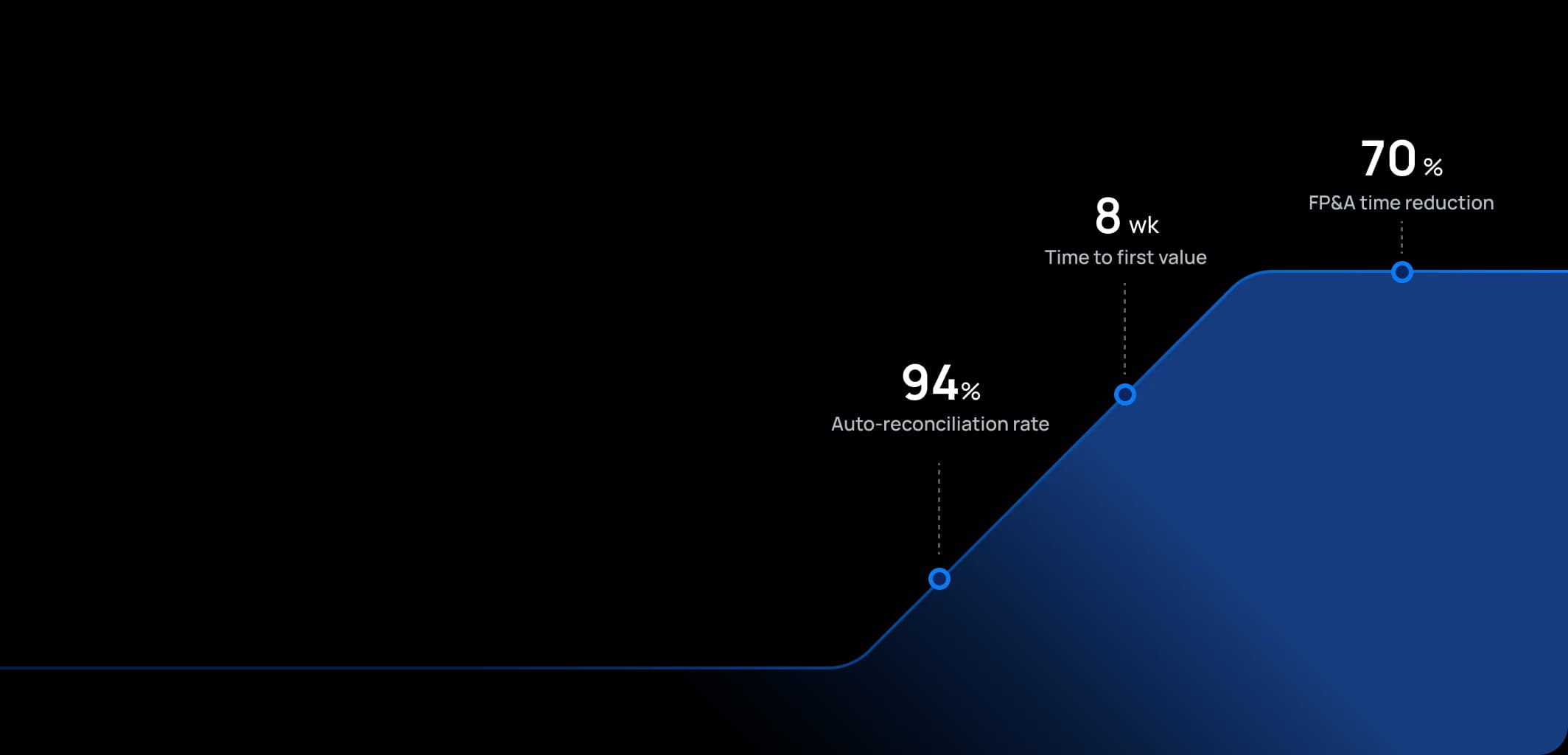

Time to first value

Man-days saved per year

Faster than spreadsheets

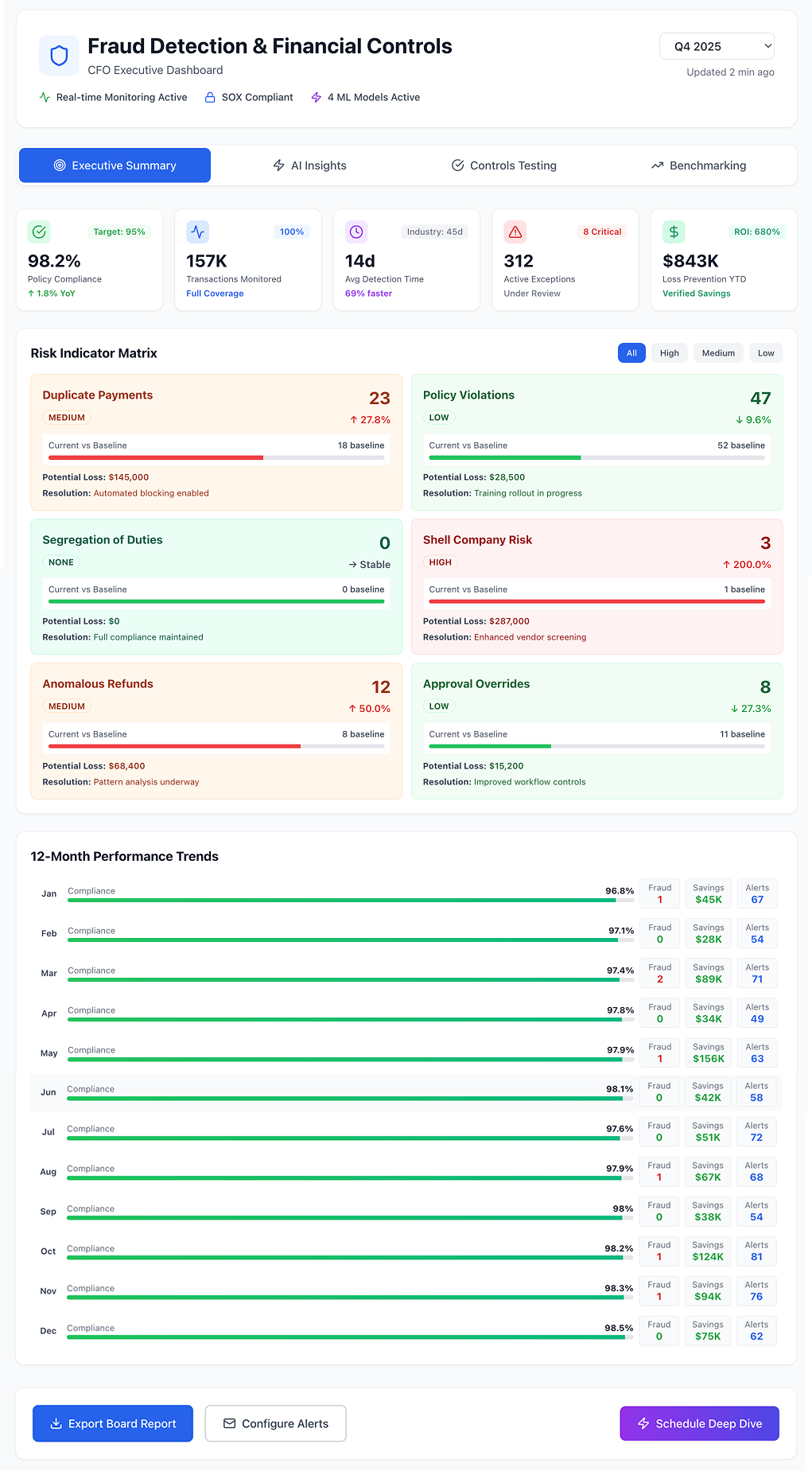

Dashboard shown is a conceptual example. Keboola integrates with any BI or analytics platform.

Dashboard shown is a conceptual example. Keboola integrates with any BI or analytics platform.

Overview

What this use case actually does.

Plug into what you already run

Your ERP, CRM, planning tools, warehouse — connected without replacing anything.

Governed, not glued together

Versioned transformations, lineage, and audit trail — every number traces to source.

Live in 8 weeks, owned by your team

Not a black box — your team configures, extends, and runs it from week one.

Safeguard assets by automatically detecting anomalies in financial transactions and enforcing internal controls in real-time.

Organizations lose an estimated 5% of annual revenues to fraud, with the average case costing $1.7 million and taking 12-18 months to detect. This use case protects your financial data by scanning all transactions (AP, AR, expense reports, payroll) for fraud signs or control violations in real-time. It serves internal audit teams, controllers, and risk officers by providing an "always-on" watch over financial processes – like having a tireless auditor who checks 100% of transactions instead of the traditional 1-5% sample. For industries with high transaction volumes (retail, banking) or fraud risks (consumer finance, manufacturing procurement), this transforms fraud detection from periodic sampling to comprehensive, continuous monitoring. The result: catch fraud in days instead of months, reduce control testing costs by 60-80%, and protect your organization's reputation and assets before losses escalate.

The pain

Where the spreadsheet breaks.

These are the problems your team runs into every month — without a unified data layer, every workaround eventually fails.

Fraud Goes Unnoticed for Months

Traditional sampling catches issues well after losses occur – if at all. Duplicate payments, fictitious vendors, inflated expenses, and kickback schemes slip through when you're only checking 1-5% of transactions quarterly. The ACFE finds frauds typically run 14-18 months before detection, often discovered by accident rather than proactive controls.

Expensive, Limited Control Testing

SOX 404 compliance teams spend enormous resources manually testing controls (checking signatures, approvals, segregation of duties) on small samples, typically at 3-4x the cost of automation

Policy Violations Multiply Unchecked

: Companies establish policies (no employee-vendors, no weekend wire transfers, expense submission deadlines) but can't enforce them without systematic monitoring.

Reputational and Financial Catastrophe

Undetected fraud creates cascading risks: direct losses, regulatory penalties, financial restatements, stock price crashes, destroyed stakeholder trust, and executive liability. A single fraud scandal can damage reputation for years

What Keboola does

What Keboola actually delivers.

No magic, no replatforming. Just connectors, governed transformations, and outputs your team owns from day one.

100% Transaction Coverage

Keboola ingests all transactions across systems (ERP, banking, expenses, procurement) and tests every single one – not just samples. It flags duplicate invoice numbers, expense amounts just below approval thresholds, vendor banking changes before large payments, and cross-references vendor files with employee databases to detect shell companies or conflicts of interest.

AI-Powered Anomaly Detection

Beyond rule-based checks, machine learning models spot statistical outliers indicating new fraud schemes: small vendors suddenly receiving 10x larger payments, unusual refund spikes by specific employees, journal entries posted at 2 AM on weekends.

Real-Time Alerts & Case Management

When issues are detected, immediate alerts go to relevant stakeholders: "High Priority: Possible duplicate payment to Vendor X, $50,000 – requires immediate review." Integration with ticketing systems (ServiceNow, Jira) converts alerts to documented investigation cases with ownership, ensuring accountability.

Automated Compliance Reporting

Generate comprehensive control compliance reports testing 100% of transactions: "Out of 5,000 purchase orders, 3 had missing approvals – details here," or "All 2,847 journal entries over $10K properly segregated except 1 instance."

Connectors

Out of the box. No replacements.

This use case typically uses 8 connectors. Keboola ships 700+ more for the long tail.

Tangible deliverables

What lands in your team's hands.

Each role gets the format and the detail they need — already configured. Not slideware.

Internal Auditor

Dashboard showing key control indicators: segregation of duties violations, late reconciliations, unauthorized vendor changes, duplicate payment alerts with investigation status. Exception reports with all flagged transactions, filterable by risk level and area, with instant drill-down to source documents and approval trails.

CFO/Controller

Executive summary of fraud cases detected (financial impact and remediation), compliance statistics (98.7% policy compliance rate), heat map showing departments by exception count, and trend analysis for Board/Audit Committee reporting. Provides assurance that controls are strong and risks managed proactively.

Accounts Payable Manager

Weekly actionable reports: "5 vendor payments flagged for review (potential duplicates or outliers) – investigate within 3 days," plus process improvement suggestions like "15 open POs inactive for 12 months – consider closing." Makes process owners active partners in the control environment rather than feeling policed.

Talk to a

real human.

No bots, no SDR call sequence. A solutions engineer who runs use cases like this every single day.

Questions & answers

Things people always ask.

Everything your team, IT, and procurement will want to know — up front.